📣 Wall Street Rallies, Aluminum Breaks Out, Nvidia Hits $5T ⚙️ Are You Positioned?

In under 5 minutes, let us introduce you to investing opportunities found in recent market analysis. Grow your portfolio with knowledge.

Edition #131

Investing Unlocks: How to Capitalize on the Hot Topics From The Last 7 Days

We analyze recent trends and opportunities, offering strategic insights that help you manage risks and identify growth opportunities for your portfolio.

📈 Markets Rally on Trade Hopes

U.S. stocks climbed to new highs for the week ending Oct 31 as solid tech earnings, easing inflation, and fresh optimism over China–U.S. trade progress lifted sentiment. Tech and consumer discretionary led gains, while defensive sectors lagged. The Fed cut rates by 25 basis points but Chair Jerome Powell emphasized that another cut in December is not a done deal, pushing Treasury yields and the dollar higher. Despite the upbeat tone, growth surveys pointed to cooling momentum, hinting that the rally may be running ahead of fundamentals.

The coming week brings key updates on manufacturing and services activity from ISM and S&P Global, along with ADP’s private payrolls report and fresh consumer confidence data. The ongoing government shutdown is delaying official releases, making private indicators more influential for market direction.

While a soft inflation backdrop and stronger trade tone are supporting risk appetite, but markets remain sensitive to any signs the economy is losing momentum.

PRESENTED BY CANTERRA MINERALS CORP.

Canterra Minerals (TSX-V: CTM, OTCQB: CTMCF) is advancing a fully-funded 10,000-metre drill program across its 55 km copper-gold corridor in Newfoundland.

Get all the details in our in-depth investor guide.

Download the Exclusive Investor Report.

Hot Topics

Tech earnings boost U.S. futures on final October trading day

Trump Cuts Fentanyl Tariffs, Secures Rare Earths Deal with China

Why Copper’s Supply Crunch is Becoming a Bull Market Catalyst

Wealth Watch

Investing Data Story

Energy spending stays dominant, but AI investment is growing 160% by 2030. What retail investors need to know about both megatrends.

AI Growth Surges as Energy Spending Holds Strong

Injectables Move From Clinic to Bathroom

Indomo, a health-tech startup founded by ex-Medtronic exec Rick Bente, is developing ClearPen, an at-home cortisone injector for acne. Backed by $25 million in funding from Atomic Labs (creator of Hims & Hers) and advisors from Allergan (Botox’s parent), the device aims to make dermatologist-grade acne care accessible without an office visit.

While still in trials, ClearPen taps into two fast-growing trends, the consumerization of medical treatments and the rise of at-home injectables driven by GLP-1 drugs like Wegovy. If successful, Indomo could position itself at the intersection of telehealth, skincare, and medtech convenience.

For small-cap investors, this is an early look at a potential category disruptor. Indomo’s model reflects how biotech and beauty-tech are converging, offering opportunities for those tracking pre-IPO medtech startups or publicly traded enablers in the at-home healthcare space (think device makers, telehealth platforms, or consumer health funds).

ClearPen’s success could signal a new wave of consumer-friendly medical devices, although not investable yet, this is a theme worth watching for early-stage or micro-cap investors hunting in the healthcare innovation niche.

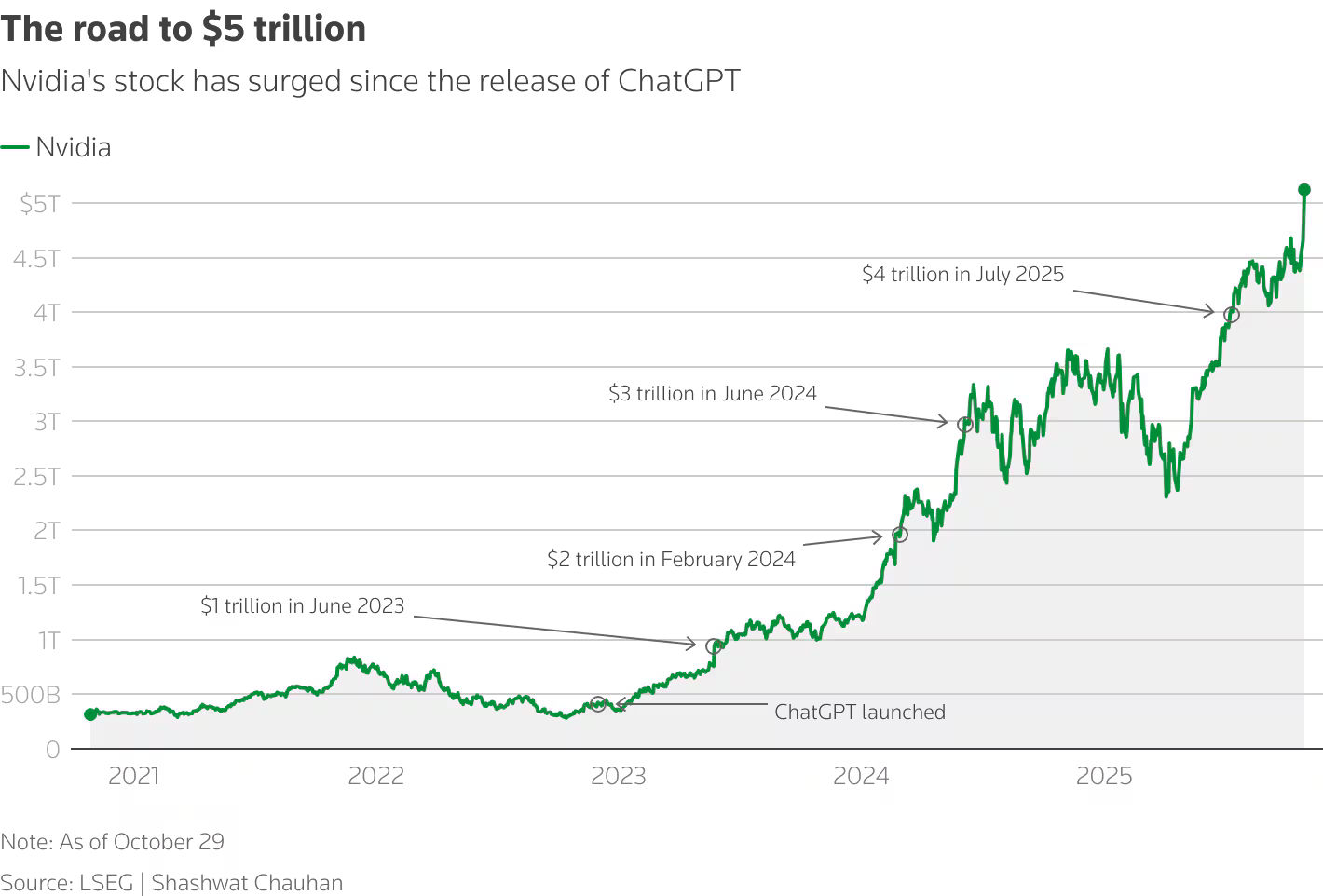

Nvidia Becomes World’s First $5 Trillion Stock

NVIDIA Corp (NASDAQ: NVDA) has become the first company in history to reach a $5 trillion market valuation, propelled by surging global demand for its AI chips and infrastructure. The milestone underscores Nvidia’s central role in powering the AI revolution, with massive new orders and partnerships driving its stock to record highs.

For investors, the achievement marks both validation of Nvidia’s leadership and a reminder that expectations are now exceptionally high.

North America’s Supply Chain Power Shift

As global trade realigns, North America is emerging as a hub for critical minerals, manufacturing and energy infrastructure. Securing regional supply chains could drive the next decade of growth — and open new investment opportunities.

Get the free report to see where capital is flowing.

Earnings Performance

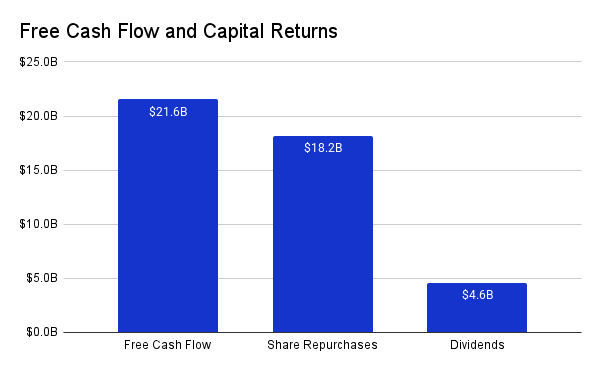

Visa Inc

Visa Inc (NYSE: V) ended fiscal 2025 with another year of exceptional cash generation, underscoring the strength and consistency of its business model. The company produced $21.6 billion in free cash flow, supported by steady growth in payments volume, cross-border transactions, and processed activity.

This financial power enabled Visa to return a record $22.8 billion to shareholders, including $18.2 billion in buybacks and $4.6 billion in dividends throughout full-year 2025.

Other Earnings Updates

AbbVie Stock (ABBV): AbbVie Beats Q3 EPS Estimates with $1.86 Results

Chevron Stock (CVX): Chevron Q3 2025 earnings beat estimates

Charter Communications (CHTR): Charter Misses Q3 Estimates

OneMain Holdings Stock (OMF): OneMain Holdings Reports Strong Q3 2025

Fiserv Stock (FI): Fiserv Shares Plunge 44% Following Earnings Miss

Investing Data Story

Investors are flocking to junior copper miners this year; the NSCOPJ is up about +70 % YTD, nearly double the performance of senior miners, as the electrification and renewables boom puts copper front and center.

From Exploration to Outperformance: Copper Juniors’ Breakout Year

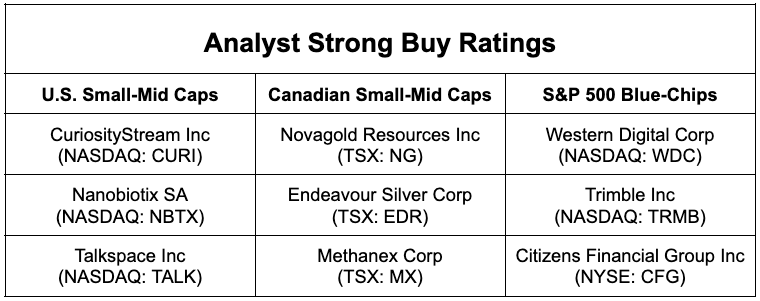

Analyst Strong Buy Ratings This Week! 📈

Looking for stocks with strong analyst backing? These companies have earned top-tier "Strong Buy" ratings from analysts, signaling potential upside for investors.

Whether you’re eyeing small-to-mid cap opportunities in the U.S. and Canada or want to stick with trusted S&P 500 blue-chip picks, this list highlights stocks that experts believe could outperform.

🔍 Do your research and see if any of these fit your portfolio!

Aluminum Joins Gold and Copper in the Spotlight

While gold flirts with records and copper surges on electrification demand, aluminum is quietly breaking out. Prices are near a three-year high of $2,900/ton.

Global supply is tightening. China produces ~60% of the world’s aluminum and has hit a domestic cap of 45 million tons. Europe’s high power costs are forcing smelter shutdowns.

To fill the gap, Chinese firms are building massive smelters in Indonesia. That’s bullish for prices, even if China ultimately finds a way to skirt its cap.

Aluminum is quietly positioning itself as a contrarian play on energy, electrification, and industrial reshoring, alongside gold and copper.

The $5T valuation arrives exactly when Blackwell demand is outpacing supply by quarters, not weeks. The Samsung GPU partnership mentioned earlier reinforces that NVDA's real moat isn't just the chips but the entire CUDA ecosystem locking in enterprise buyers. With hyperscalers planning 2026-2027 capex budgets now, the multiple might look stretched at 35-40x earings, but the forward order book suggests the denominator keeps expanding faster than the numerator compresses.